July 25, 2025

The One Big Beautiful Bill Act is now law, and trade deals and tariff strategy are increasingly clear. Volatility in major equity indexes has returned to pre-tariff levels, and values have started to climb as GDP growth is anticipated. The consumer is confused. We have a debt problem to deal with.

Markets steady as policy uncertainty recedes

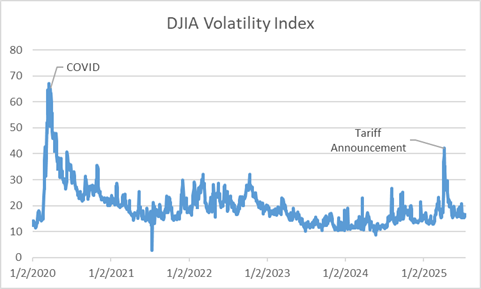

After briefly spiking on tariff announcements, the volatility indexes for the Dow, Nasdaq, and S&P 500 have all returned to their long-term averages. (Figure 1) While never reaching pandemic levels of risk concern, the indexes nevertheless reflected market uncertainty around tariff and tax policy. With the passage of the One Big Beautiful Bill Act, investors and businesses believe they understand the regulatory and tax environment. Year-to-date returns on the Dow, Nasdaq, and S&P 500 are all positive, at 4.6%, 8.1%, and 7% respectively.

Consumers confused, but strong

Unlike institutional investors and publicly traded companies, consumers are still confused. Lacking the ability to put tax policy and tariff policy gyrations into perspective, a flight to a pessimistic outlook seemed safe.

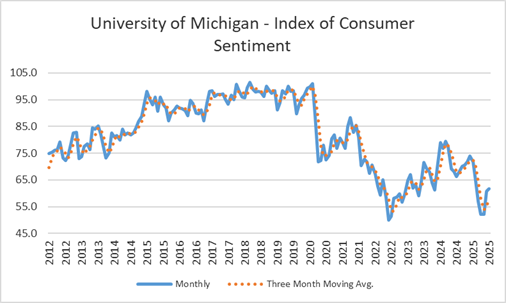

However, after dropping sharply in April, sentiment has begun to rebound and become more aligned with the reality on the ground. The consumer's mood improved in June, and preliminary July numbers show modest continued improvement. (Figure 2)

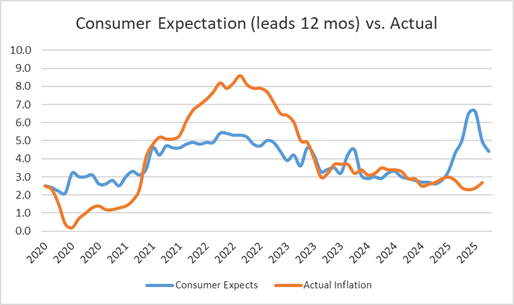

Consumer expectations of inflation began rising in February due to tariff fears and moved dramatically higher through May, reaching 6.6%, a level not seen even at the height of post-pandemic inflation. (Figure 3) However, while slower to react than equity volatility indexes, consumers have begun to understand they overestimated inflation concerns, and expectations moderated significantly in May and June. Meanwhile, inflation climbed modestly in May and June as tariff pricing percolated through the economy and energy deflation moderated. Soon, we will return to an inflation environment that meets the consumer's expectations.

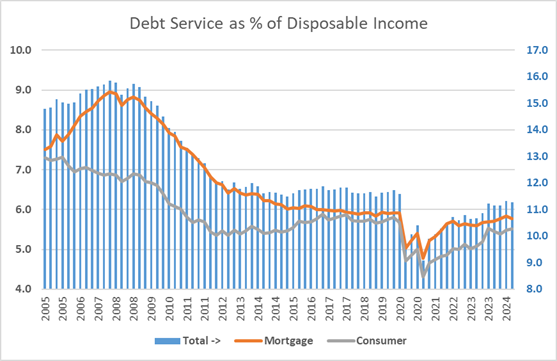

Retail sales continue to show strength, a byproduct of a strong, de-leveraged consumer. After a long, painful de-leveraging period following the Great Recession, consumers maintained a stable and sustainable level of debt leading up to the pandemic. Taking advantage of generational low interest rates, consumers once again de-leveraged, and this time it was quick and painless. Millions locked in low, fixed-rate mortgages, which have served as a household hedge against inflation. This has enabled the home-owning consumer, specifically, to maintain a sound financial condition and this continues to fuel spending that drives economic growth. (Figure 4)

Housing demand and supply in Washington

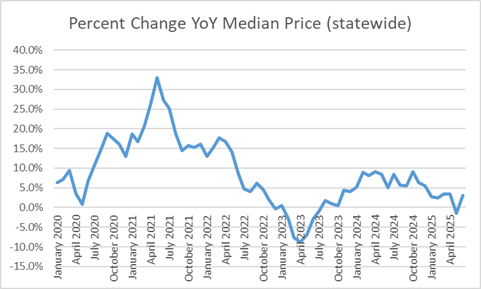

Across Washington state, buyer demand remains solid, but elevated mortgage rates and sticky prices have constrained transactions. Many renters want to buy, but affordability remains the obstacle. Price growth has slowed throughout the first half of 2025, while inventory is growing modestly and showing seasonal price softening. (Figure 5)

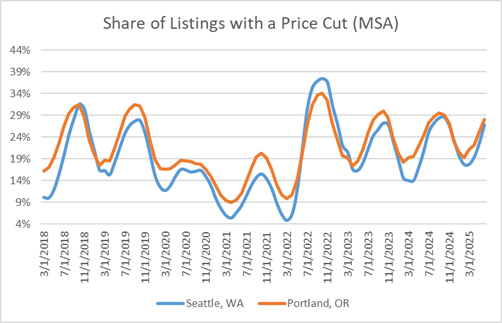

Comparing the Seattle MSA to Portland, Oregon (which includes SW Washington), the share of inventory with a price cut is elevated on a seasonal basis, but not outside historical levels or the highs of 2022, as interest rates rose rapidly. (Figure 6)

Inventory is now approaching 2019 levels, with a 20% increase YoY compared to mid-2024. (Figure 7) However, conditions vary by metro—some areas exceed pre-pandemic supply while others remain below. Pricing pressures are beginning to stabilize, signaling neutral pressure on statewide values.

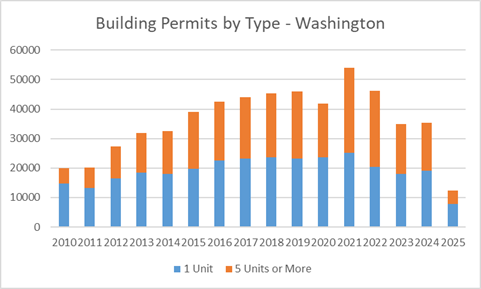

Permitting activity forecasts a 8–12% decline in total units for 2025, with a sharper pullback in multifamily starts. In contrast, single-family permits are projected to make up 58% of new housing this year—up from 50% in 2024—indicating a shift in builder focus as multifamily demand and financing conditions cool. (Figure 8) The adjustment to supply has already begun.

Government debt is a challenge

With policy volatility now behind us, the looming fiscal concern is debt management. While proponents argue the new legislation is deficit-neutral, that remains to be proven. The more immediate issue is the need to roll over existing debt at today’s higher rates.

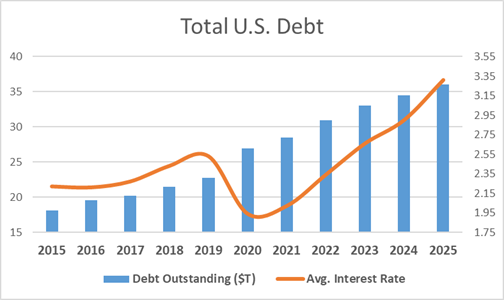

More present is the need to "roll over" existing debt. Since 2015, absolute debt has increased by nearly 98%, while borrowing costs have risen by 70% since 2020, marking an unsustainable trajectory. (Figure 9)

Debt to be refinanced, along with new spending, reached almost $13 trillion in 2024 and is expected to continue at a pace of $9 to $12 trillion for the next several years. (Figure 10) The implication for housing is the influence this will have on the yield of 10-year U.S. treasuries. Without moderating interest rates, increases in transaction velocity will take much longer to achieve, and pricing pressure will remain.

Looking ahead

The approach to monetary and fiscal policy is much clearer at the halfway point of the year. Markets have adjusted and volatility is at normal levels. Consumers are beginning to understand how to act, and expectations are aligning with reality, while job growth remains above the absolute level needed to maintain the current rate of unemployment.

GDP growth and sustained job gains, coupled with additional trade stabilization, would go a long way toward unlocking pent-up housing demand and returning transaction volumes to pre-pandemic levels—potentially 750,000 to 1,250,000 additional annual sales needed to reach long-term averages.

BIAW has teamed up with WFG National Title Insurance Company’s Noah Blanton to offer quarterly economic forecasts to assist members in making decisions for their businesses. Contact him for more information at (503) 431-8506 or nblanton@wfgtitle.com.